Private sector; know your obligations in relation to IR35

From 6 April 2020, if a company uses an individual / a contractor (usually through a personal service company (“PSC”)) who provides services to a company then the onus will be on the company to assess whether an individual working through a PSC would have been regarded as an employee if they were engaged directly by the company (i.e. the fee payer) and not through a PSC. If, after an assessment, the answer is YES then it will usually be the company who will be obliged to deduct and account for income tax and NICs on the monies that it pays to the PSC (IR35 will be applicable).

At the outset, from 6 April 2020, the rules will only apply to medium and large companies in the private sector, so small businesses will not be required to operate the new rules at this stage albeit, our advice is that, it is best practice for all companies to consider the arrangements that they have in place with respect to any contractors / PSCs.

At present, and until 6 April 2020, the onus is on the individual to assess the relationship between them and the company and, if necessary, pay income tax and NICs on the monies received from the arrangement.

The key points which companies should consider in relation to IR35:

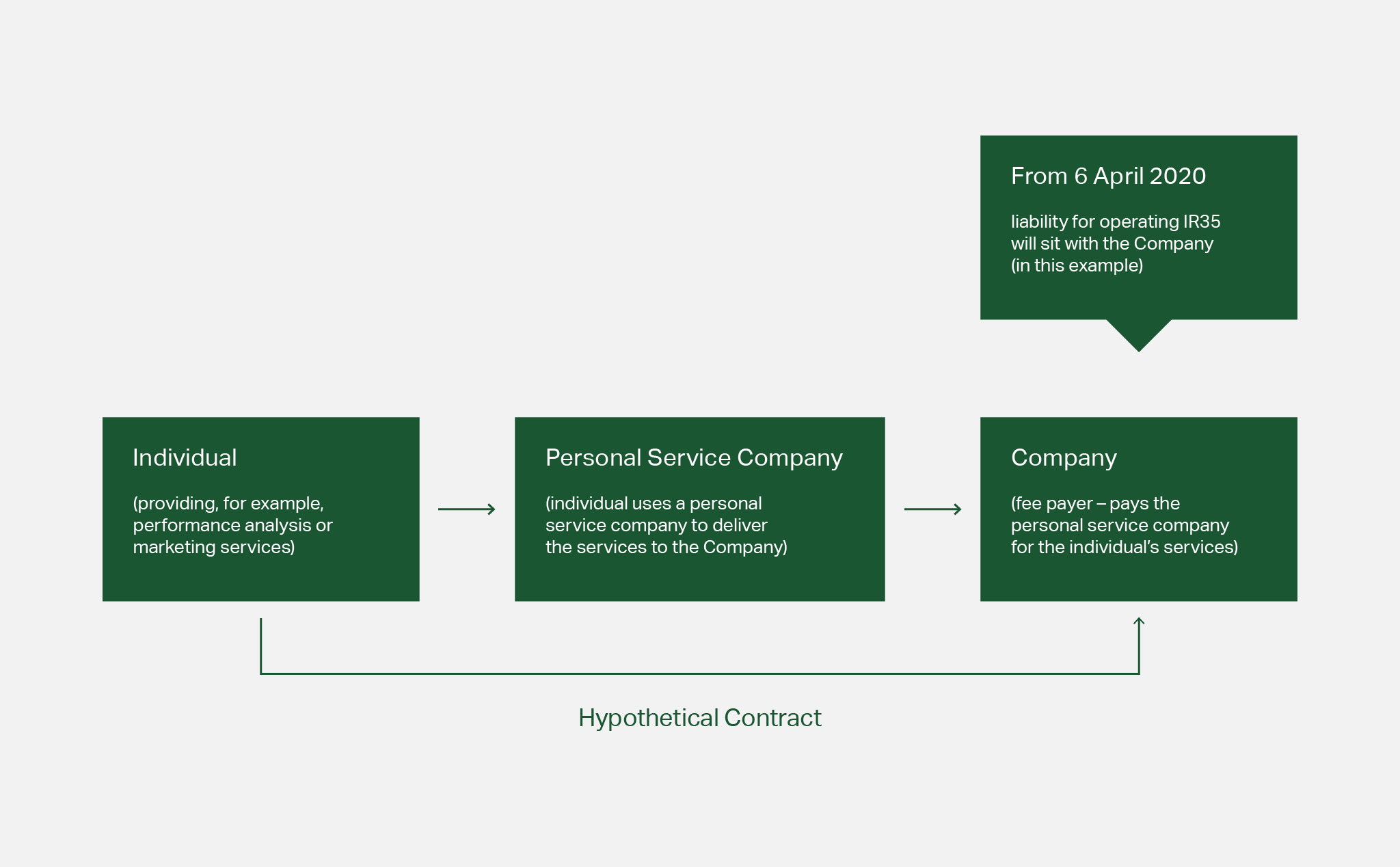

#IR35 Rule – the IR35 rules only apply where there would have been an employment relationship between the engaging company and an individual (i.e. a contractor) if the individual had engaged directly with the company, rather than through an a PSC. The IR35 rules do not apply where there would have been a genuine self-employment/consultant relationship. If challenged, a Tribunal will construct a hypothetical direct contract between the individual and the engaging business (it will disregard the PSC for this purpose) to ascertain whether that hypothetical contract would be one of employment or self-employment. Until 6 April 2020, if IR35 applies, in the private sector, the onus is on the contractor to assess the arrangement and pay income tax and NICs on the monies received from the arrangement (if applicable).

#From 6 April 2020 – the onus will be on the party who pays the PSC to assess the arrangement and HMRC will be able to go to that party, which will usually be the company, to challenge whether income tax and NICs should be payable. If it is deemed that income tax and NICs should be payable then it would be payable by the party who pays the PSC. However, if a company is not the fee payer (i.e the company uses a staffing agency and the staffing agency pays the PSC) the company can still be liable to pay the income tax and NICs (so using a staffing agency, for example, will not necessarily extinguish a company’s liability).

#HMRC guidance – in determining whether IR35 applies, HMRC has developed guidance on when it considers an employment relationship exists (but HMRC has acknowledged the results generated from this guidance are not always accurate). Further, there could be situations where part of an arrangement could be deemed to be a genuine self-employment/consultancy arrangement and part of it could be more akin to an employment relationship. The onus is on the party who pays the PSC to ensure that it assesses the situation and pays the correct income tax and NICs on the sums or any proportion of the sums attributed to an employment relationship.

#Tribunal determination of employment status – in determining whether, in reality, an individual would be an employee, Tribunals typically look at whether there is the following:

- #Mutuality of obligations – between the individual and the company (i.e. is the company obliged to offer work and is the individual obliged to accept it?);

- #Control – does the company have a sufficient degree of control over the individual (i.e. what degree of control does the company have over what, how, when and where the individual completes the work?);

- #Substitution – is there a right of substitution (i.e. is personal service by the individual required or can the individual send a substitute in their place?); and

- #other terms – other terms not inconsistent with a contract of employment.

#Next steps – companies should consider the following in terms of next steps:

- #Due Diligence – companies should review its ongoing arrangements to identify how many contractors (and, if applicable whether there are any staffing agencies) it engages and undertake a comprehensive risk assessment to establish its exposure to IR35 and what changes need to be made;

- #Current arrangements – it may be appropriate and necessary for companies to negotiate new terms or arrangements with current contractors (and staffing agencies if they use any), to ensure that companies have the necessary protection in the event that HMRC deems that income tax and NICs are payable in relation to an arrangement; and

- #New arrangements – care should be taken to ensure that any new arrangements which the company enters into from 6 April 2020 has the necessary protection in place from the outset for the company.

If you would like more information on any of the points raised above or any advice in connection with the same, please contact Helen Littlewood (Associate) – HelenLittlewood@centrefield.law – or call 0161 672 5450.

Please note the information contained in this briefing is intended as a general review of the subject featured and is not intended as specific legal advice.